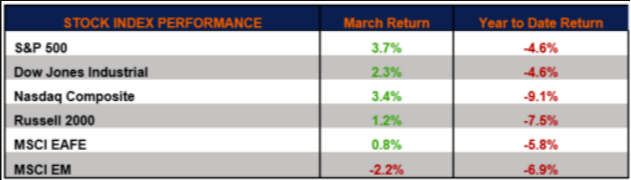

During March most equity markets worldwide gained ground, reversing two straight months of declines. The present geopolitical tensions in Eastern Europe have added to the market’s “wall of worry”. This on top of inflation concerns, along with corresponding Federal Reserve monetary policy, caused markets to get over-pessimistic. Thus, buyers took advantage of marked-down equities. Solid gains were seen throughout the major U.S. equity indexes in March.

As we continue through the economic recovery, battling through the remnants of COVID-19, the present geopolitical struggle in Eastern Europe has investors concerned about the global economic output. On top of this, inflation is proving stickier than many anticipated. The Fed’s hawkish view, along with the bond market, has affirmed this.

Market participants are presently weighing the effects of all these factors, leading to higher volatility in financial assets. Presently, amid these challenges, S&P 500 Index company fundamentals appear intact. Q1 earning reports will provide a clearer view of company as well as supply-chain fundamentals. Our base case continues to be that inflation should begin to stabilize once supply chains are fully operational and labor shortages ease. In addition, in our view, the health of the consumer should continue to be an important driver for the economy and corporate profits in 2022.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. All market and index data comes from FactSet and MarketWatch.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

This Research material was prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).